Uncategorized Archives - Alternative Energy Stocks

https://altenergystocks.com/archives/category/uncategorized/

The Investor Resource for Solar, Wind, Efficiency, Renewable Energy StocksMon, 23 Nov 2020 16:43:30 +0000en-US

hourly

1 https://wordpress.org/?v=6.0.9Happy Thanksgiving

https://www.altenergystocks.com/archives/2020/11/happy-thanksgiving/

https://www.altenergystocks.com/archives/2020/11/happy-thanksgiving/#respondMon, 23 Nov 2020 16:43:30 +0000http://3.211.150.150/?p=10769Spread the love I hope everyone is having a happy Thanksgiving, and, more importantly, staying safe by keeping your gatherings small and staying close to home. Next year, it looks like we will have multiple, highly effective vaccines. Just like in the market, this holiday season, the waiting is the hardest part. Tom Konrad, Editor

I hope everyone is having a happy Thanksgiving, and, more importantly, staying safe by keeping your gatherings small and staying close to home. Next year, it looks like we will have multiple, highly effective vaccines.

]]>https://www.altenergystocks.com/archives/2020/11/happy-thanksgiving/feed/0North American Outlook on Biofuels Challenges and Opportunities

https://www.altenergystocks.com/archives/2019/11/north-american-outlook-on-biofuels-challenges-and-opportunities/

https://www.altenergystocks.com/archives/2019/11/north-american-outlook-on-biofuels-challenges-and-opportunities/#respondSun, 10 Nov 2019 14:55:52 +0000http://3.211.150.150/?p=10149Spread the love Challenges and Opportunities in Biofuels By Steve Hartig, Former VP of Technology Development at ICM The North American biofuels market can be split into three main segments all of which have major dynamics. What I would like to do is give a high-level overview of what I see as some of both the challenges […]

By Steve Hartig, Former VP of Technology Development at ICM

The North American biofuels market can be split into three main segments all of which have major dynamics.What I would like to do is give a high-level overview of what I see as some of both the challenges and opportunities across these.

Ethanol which is a produced from corn and sorghum in about 200 plants mainly across the Midwest and blended at about 10% with gas.Majors such as POET, Green Plains, Flint Hills, Valero, ADM and Cargill do a bit more than half of the 16 billion gallons production with the rest done mainly by farmer co-op plants.An average plant size is about 80 mln gpy.About 10% of gasoline is ethanol. Cellulosic ethanol is the newer area which has had many challenges but companies such as POET DSM are producing some volumes from crop residues and Lanzatech from gas streams.

Biomass based diesel produced mainly from vegetable oils and waste fat in a large number of plants, typically rather small, across the US with the market leader being REG.Total volume sold in the US, per the EPA was 2.3 bin gallons, in 2018 or about 4-5% of the total diesel supply.Actual capacity is much larger at 4.1 bln gallons.

Bio jet fuel which is still embryonic but an interesting are with about 25 bln gallons of potential.What is exciting is that this area is likely to grow in volume over time and alternative approaches such as electrification are difficult for aircraft given the weight of batteries so this is a long term and growing market for biofuels

Challenges for the corn ethanol and biodiesel producers are very much around profitability and the regulatory environment while the embryonic cellulosic and jet fuel areas still has many technical challenges to prove viability.

Corn Ethanol

There is a huge challenge today due to oversupply versus demand driving prices down.There is much arguing as to the cause of this but it seems to be a combination of low or no growth in gasoline demand, significantly added ethanol capacity, a slow uptake of higher-level ethanol blends and the EPA Small Refinery Exemptions.This is aggravated by the dynamics in corn pricing this year due to weather.

Unless E15 volume increases significantly, things are only going to get worse as essentially all forecasts show gasoline volume decreasing over the coming five to ten years driven by increased fuel economy in the short run and vehicle electrification in the long term.

Forecasting what will happen is difficult as ethanol is very different than most commodity chemicals due to the relatively small plant size, driven by corn supply economics, and the large number of companies active in it.In most commodity chemicals markets, a handful of companies control the market and new entrants are difficult due to the lack of economies of scale.However, continued consolidation and the closing of smaller, less efficient and poorly located plants will continue.

The starting point for surviving any downturn and long term sustainable profit will be having a plant with a low cost position driven by a combination of scale, plant technology, location, operational excellence and strong maintenance.The difference between leaders and laggards here can be over $.10 per gallon, which is huge.

However, the likely winners will be those that also embrace some form of specialization next to the commodity markets for ethanol, distillers grains and corn oil.

A number of options exist and this is also an exciting area of focus for many companies.

Main areas include:

Moving towards higher value animal feed by fractionating the distillers grains into more focused animal feeds. Options for this exist from many suppliers including ICM and Fluid Quip Process Technologies.Both companies take an approach of splitting the DDGS into two streams, one a high protein feed product targeted at poultry, swine and aquaculture and the remainder being either a DDGS at the low end of the protein specification or a wet fiber and syrup product targeted at cattle. The value comes from the fact that the higher protein product more competes with soy rather than corn andcan capture a higher price.Both companies have multiple installations in place and claim paybacks in the 2-4 year range.Considerations for installing these technologies would include plant scale and geographic location with proximity to cattle allowing the use of wet feed an advantage.

Towards the future, options will include using stillage as a fermentation broth such as both White Dog Labs and KnipBio are developing.Both companies are focused on using the relatively inexpensive stillage to produce single cell proteins aimed at aquaculture.These products can potentially compete with fish meal which a$1500/ton and is also limited in growth potential. White Dog Labs has announced an initial installation in Nebraska while KnipBio has announced a cooperation with ICM towards commercializing their technology.

Focusing on California and the increasing low carbon fuel markets.Today, with the value of a carbon credit close to $200, a plant with a CI of 75 can get a premium of over $.25 per gallon.There are only a few plants in the 60’s but many in the mid 70’s.Typical approaches include alternative power sources such as land fill gas or anaerobic digestion to biomethane combined with cogeneration of electricity and steam.Other options include solar or biomass boilers.A newer approach is the use of membrane technology to reduce the energy used in the molecular sieves or alternatively modifications to the evaporators.The keys when considering this approach would include a good starting point with plant efficiency and the cost of west coast shipment.

Using the ethanol plant as a platform to produce other products.Edeniq has a number of plants producing cellulosic ethanol from corn fiber while both ICM and D3Max have their first, larger scale, plants under construction. Cellulosic ethanol from corn fiber is much lower cost to produce than cellulosic ethanol from crop residues or energy crops.Edeniq has no capex and claims a cellulosic ethanol amount of 3-4% while both D3Max and ICM indicate levels more in the range of 7-8% but have significant capital. However, the payback can be short given a combination of a D3 RIN and potential LCFS credit.Another alternative in the future may be butanol with Gevo (NASD:GEVO) and Butamax both having demonstration facilities up and running.

I believe these options will be a game changer for the industry but companies must make the right choice based on starting position, plant location, scale and technology, risk tolerance, operational capabilities and capital availability.A key item for many of these is that they will typically create a more complex plant and business environment which can require a higher level of staffing, capability and management expertise.

I think the future can be bright for ethanol but I foresee a future that likely has fewer, larger and more sophisticated plants than are in place today.

Biomass based diesel

Biomass based diesel (BBD) has very different dynamics with about 100 plants in the US, some of which are very small, less than 10 mln gallons per year.Many of the plants are driven by location by feedstocks, either soy or corn oil or waste fats and greases.Demand for BBD is very much driven by the RFS as it typically costs more than petroleum-based diesel but can fulfill either the D4 BBD RIN or the Advanced D5 RIN.This is particularly the case with the biodiesel tax credit lapsing in 2017 and, at least so far, not being renewed.

The big change going on now is the shift towards renewable diesel, presently about 15% of total BBD, which is more costly to produce but is essentially a drop in for diesel and can have lower carbon numbers, depending on feedstocks.Due to the lower CI it is being heavily targeted at California for sale under the Low Carbon Fuel Standard.In addition, it can capture a greater RIN value.

The plants scheduled to come on line over the next few years is mind boggling given today’s position.Expansions planned or proposed by Diamond Green (a joint venture between Darling Ingredients (DAR: NYSE) and its joint venture partner Valero Energy (VLO: NYSE)), NEXT Renewables, RYZE, Philips 66 (NYSE:PSX)/Renewable Energy Group (NASD:REGI) and others could add up to 2 bln gallons of new Renewable Diesel volume focused on West Coast markets and almost doubling the total volume of BBD volume.This is in addition to global expansions in biodiesel by companies such as Neste and companies coprocessing it in oil refineries.

Selected US Renewable Diesel Projects

Scale (mln gpy)

Location

Timing

Status

NEXT

550

Oregon

2022

Permitting

Phillips 66/Ryze

160

Nevada

2019-20

Under Construction

Diamond Green

400

Louisiana

2021

Under Construction

World Energy

260

California

2021

Under Construction

REG/Phillips 66

250

Washington

2021

Planning

Note:Project information from company websites and public announcements

This will have significant impacts on the market:

The total diesel fuel market is not expected to grow much, per the EIA, so this fuel will need to displace petroleum-based diesel which may negatively impact pricing. There also is more capacity than there are RINs available which will have a downward impact on that.On the plus side, is the LCFS which is spreading beyond California and will bring a carbon credit.REG indicated in their 10k that the 2018 value was between $.40-.80 per gallon.

Regulation unclarity will continue between the RFS volume obligations, tax credits, trade policy, and the Small Refinery Exemptions which appear to have more impact on BBD than ethanol.Right now, several smaller BBD producers are not operating due to lack of profitability.

How about feedstocks?Right now BBD uses a combination of soy oil, corn oil and waste fats and greases.BBD today uses about a third of the US soy oil supply so this will clearly impact pricing and availability certainly in the shorter run.What will aggravate this is that all the feed streams are byproducts of other processes so cannot be increased on their own along with all the dynamics hitting soy on the trade side.The EPA in their draft 2020 RVO estimates that from 2019 to 2020 feedstock availability would be enough to produce about 144 men gallons of advanced biodiesel and renewable diesel.

I think this business will continue to have challenges in the future and it is also likely not all the plants proposed will be built but the trend towards renewable diesel will continue.

Bio-jet Fuel

Bio jet fuels have a completely different environment that ethanol and biodiesel both as they are presently not mandated by the government and also as they are in an earlier stage of technical development.

There are three broad technology areas that cover much of the effort.Most technologies would produce a fuel that could be blended at some level with standard jet fuel.

Renewable diesel/oil to jet—This process is an additive process to biobased diesel taking the diesel and cracking it, isomerizing it and then purifying the end product.

Alcohol to jet—Basically taking an alcohol, either ethanol or butanol, and then dehydrating it to remove the extra oxygen and then catalytically or chemically converting this to jet fuel.The advantage of this is the ethanol routes are well developed so only the final process step is new.Potentially this could consume some of the excess ethanol in the market but that would likely be with a penalty to CI compared to routes such as LanzaTechs using cellulosic feed streams.Players here include Gevo, LanzaTech and Byogy.

Gas to liquids—the typical routes here are gasifying a biomass or MSW stream into syngas and then using technology such as Fischer Tropsch to convert it to jet fuel.Pyrolysis is another alternative.This is earlier stage technology but has the potential for very low carbon due to feedstocks and will have wide feedstock availability.Players here include Red Rock Biofuels and Fulcrum.

Selected US Jet Fuel Projects

Scale (gpy)

Technology

Location

Timing

Red Rock

15 mln

Wood to Syngas to Fischer Tropsch

Oregon

2020

Fulcrum

10 mln

MSW to Syngas to Fischer Tropsch

Nevada

2020

Lanzatech

10 mln

Gas fermentation to ethanol to jet

Georgia

TBD

The diesel fuel route is clearly the one with the fewest technical hurdles but will run into the same feedstock issues that biodiesel has if it moves to any significant volumes.Alcohol to jet would be the next most straightforward while it seems like the gas the liquids route has the best carbon footprint and also feedstock potential.However, it is unclear what the cost will be and what technical hurdles they will hit.

The next five years will see major learning taking place as commercial plants for many of these technologies are underway.

What makes bio jet particularly interesting and challenging is that it really is a global market so any regulations put in place by a single country could be very challenging to implement and enforce.Conversely, given the global trade environment it seems unlikely that a global pact will appear anytime soon.

Without a mandate, it appears the airlines are broadly experimenting with biofuels but not making any major commitments.My cynical view would be that they are doing everything they can to show progress while putting minimal money on the table.Given the impact of fuel prices on airline profitability and the fact today that most or all biojet fuels will be more expensive than fossil-based fuels I would guess progress will move slowly.

Looking at the RFS, the pathways exist to capture a D4 RIN for biodiesel type approaches, a D5 RIN for Renewable diesel approaches and a D7 when using cellulosic feedstocks.It does not appear that there is an existing pathway for a corn-based ethanol to jet fuel.

The question is what the RFS will do if biojet fuel grows significantly in volume as they presently define all their mandates based on surface transportation.If there were suddenly an extra billion gallons of RIN’s available without the obligated parties needing to purchase them this would crash the value of the RINs.California is working on routes within the LCFS but this presumably would be restricted to California.Overall, this could provide benefits would not want to bet a business on the availability of RINs.

Long term, I think bio jet fuel will be a large and important market but it will take some form of carbon charge or other mandate.Until that it will likely stay small.

I think today is an exciting time in biofuels, as always, with lots of dynamics and opportunities for companies to succeed but also fail.

Author Notes

Steve Hartig is an experienced executive with almost 40 years of experience across DuPont, DSM and ICM in leadership roles.He is presently acting as an advisor/consultant to companies in the biofuels and other segments.

This post first appeared on Biofuels Digest. Biofuels Digest is the most widely read Biofuels daily read by 14,000+ organizations. Subscribe here.

]]>https://www.altenergystocks.com/archives/2019/11/north-american-outlook-on-biofuels-challenges-and-opportunities/feed/0Gevo’s Soil Amendment

https://www.altenergystocks.com/archives/2019/08/gevos-soil-amendment/

https://www.altenergystocks.com/archives/2019/08/gevos-soil-amendment/#respondTue, 06 Aug 2019 15:22:13 +0000http://3.211.150.150/?p=10029Spread the love by Debra Fiakas, CFA In a series that began in March 2019, with the article titled “Vagants on the Earth,” we looked companies offering products that address the building problem of top soil degradation and loss. In the four articles that followed we explored forestation technology, environmentally-friendly timber harvesting, and modern soil fallowing programs. Unfortunately, we found […]

In a series that began in March 2019, with the article titled “Vagants on the Earth,” we looked companies offering products that address the building problem of top soil degradation and loss. In the four articles that followed we explored forestation technology, environmentally-friendly timber harvesting, and modern soil fallowing programs. Unfortunately, we found few companies where investors could get involved quickly as minority investors. Another company has joined the movement to build topsoil. This one has publicly traded stock!

Last week Gevo Corporation (GEVO: Nasdaq) announced commencement of a trial for a soil treatment at its Luverne, Minnesota facility. The treatment developed by Locus Agriculture Solutions (Locus AG) is aimed at improving soil health for greater crop productivity. Of course, Gevo is interested in improving corn crop yields for feedstock used in its isbutanol, renewable gasoline and jet fuel production. However, the nature of Locus’ soil treatment technology as a non-petroleum based fertilizer will also give Gevo bragging rights to a smaller carbon footprint.

The Rhizolizer soil solutions that is being applied to Gevo’s corn fields is one of two products in Locus AG’s technology portfolio.It is composed of fungal and bacterial microbes that learned in the earlier soil series are vital for top soil productivity.Microbes can affect soil structure and fertility by digesting organic plant matter and animal residues.They can also help transport mineral nutrients and water to plants.The product gets its name from the ‘rhizosphere’ region where soil microbes interact with plant roots and stems.

The file illustrates a root tuber colonized by an arbuscular mycorrhizal fungus. The animation has been extracted from a film on arbuscular mycorrhizal fungi. By Scivit via Wikimedia Commons.

Rhizolizer is applied through the crop irrigation system and can be tailored to a particular crop and field. So far it has been used on a variety of crops, including strawberries, citrus fruit and potatoes.

Customers with turf and shrubs can use Locus AG’s Terradigm treatment, which is a ‘brew’ of active microbial strains in a liquid. While the product must be kept refrigerated, it is highly concentrated and is applied in small amounts with a spray.

Gevo’s strategy to improve corn crop yields without using more petroleum-based fertilizer certainly should enhance the company’s ‘street cred’ for environmental sustainability and low carbon emissions. Even if crop yields do not increase at all, Gevo could benefit. First, any carbon footprint calculation could be changed in Gevo’s favor.

Second, Gevo could be recognized for carbon sequestration. That said, carbon sequestration benefits are a bit elusive. Soil is a known carbon sink. It is estimated that about one-third of greenhouse gas emissions originate from the conversion of land from grass and trees to cultivation. Working in reverse, the amount of carbon dioxide that gets caught up in soil due to an improvement in soil health is entirely uncertain.

The field trials should provide Gevo with the data to determine if the soil treatment is also economic. Improvement in crop yields at an attractive investment in soil treatment could have an impact on Gevo’s profits. Furthermore, if somehow the carbon sequestration is quantified and translated into credits that could be also have a positive impact on Gevo’s profit margins.

Gevo has still not turned a profit with its isobutanol or renewable fuel products. Investors taking a long position in its shares will have to wait at least two more years for any profits trickle to the company’s bottom line. In the meantime, the company taps its bank account for about $1.25 million each month to support operations. Thus no matter how enthusiastic an investor might be about Gevo’s latest efforts to improve the upstream end of its feedstock supply chain with improved corn crops, the shares are only for those with plenty of patience.

Neither the author of the Small Cap Strategist web log, Crystal Equity Research nor its affiliates have a beneficial interest in the companies mentioned herein.

]]>https://www.altenergystocks.com/archives/2019/08/gevos-soil-amendment/feed/0First Solar and SunPower Lobby Shareholders to Sell 8point3 YieldCo

https://www.altenergystocks.com/archives/2018/02/first-solar-sunpower-lobby-shareholders-sell-8point3-yieldco/

https://www.altenergystocks.com/archives/2018/02/first-solar-sunpower-lobby-shareholders-sell-8point3-yieldco/#respondWed, 28 Feb 2018 14:17:25 +0000http://3.211.150.150/?p=7260Spread the love1 1Shareby Tom Konrad Ph.D., CFA Will shareholders accept the deal? On Monday, 8point3 Energy Partners, the joint YieldCo from First Solar and SunPower, entered into a definitive agreement to be acquired by Capital Dynamics. When public companies are sold, it’s almost always at a premium to the market price. It’s that price premium […]

On Monday, 8point3 Energy Partners, the joint YieldCo from First Solar and SunPower, entered into a definitive agreement to be acquired by Capital Dynamics.

When public companies are sold, it’s almost always at a premium to the market price. It’s that price premium that persuades shareholders to sell. So why would 8point3 (NASD: CAFD) shareholders accept a deal that offers them only $12.35, or 15 to 20 percent below the roughly $15 price CAFD has been trading around for the past three months?

To answer this question, we need a little history.

Figure: 8point3 Energy Partners three-month stock price, via BigCharts.

Jan Schalkwijk, founder and portfolio manager at investment advisory firm JPS Global Investments, said that First Solar (NASD: FSLR) created 8point3 to unlock capital for its solar project development business.

“First Solar got into the solar project business as a means to pull demand for its panels in an over-supplied market,” said Schalkwijk. “As it turns out, First Solar was quite good at it, and many of the largest utility-scale solar plants in operation in the U.S. today are First Solar projects.”

“But operating a solar plant is inherently a different business from producing solar panels and locks up a lot of capital,” Schalkwijk added. “Also the investment thesis is different and more yield-driven than the higher risk (and higher cost of capital) product side. To free up capital and reduce the cost of capital for projects to pencil out, it formed a YieldCo, 8point3.”

He expects that SunPower’s reasons were similar.

From the point of view of solar manufacturers like First Solar and SunPower, the reason to own a YieldCo is to have a captive buyer of solar projects. Since that YieldCo could not raise money in the stock market to buy projects at attractive prices, they chose to sell the YieldCo itself.

JPS Global holds First Solar and a small position in SunPower in client accounts. They sold all holdings of 8point3 in 2017. JPS is also the manager of the Green Income Folio strategy. I am the primary research provider and joint developer of this strategy, which includes First Solar on Schalkwijk’s recommendation, but no position in CAFD.

An offer they can’t refuse

The argument for shareholders to approve the buyout amounts to: “Not the best YieldCo you got there. Shame if no one were to buy it.”

The long-term prospects for 8point3 as a standalone company are not bright. This has been apparent for some time, but the price has been going up anyway. I believe that the recent stock price strength (which has eroded since the sale was announced) arises out of mostly small investors focusing only on the current dividend without any consideration of its sustainability, while the more sophisticated investors are reluctant or unable to short the stock. Recent news headlines (like this and this) support this point.

Obviously, 8point3’s stock was risky, something I and most professional investment analysts have been pointing out for the last year. According to Yahoo, eight out of 11 analysts rated 8point3 a “Hold” or “Underperform” at the start of the month.

I personally wrote an article on Greentech Media last July, which attempted to value the YieldCo in the case of a sale. Looking at the long-term sustainability of 8point3’s cash flow, I came up with a valuation range of $8 to $13, which puts the actual offer at the high end of my range.

Significant challenges for 8point3 as a standalone public company

An investor presentation on the sale of 8point3 outlines the risks to the YieldCo’s business model, while trying to shift the blame for the company’s perilous condition onto “market conditions.” These are the same risks that professional analysts have been highlighting, but which small investors seem to have ignored.

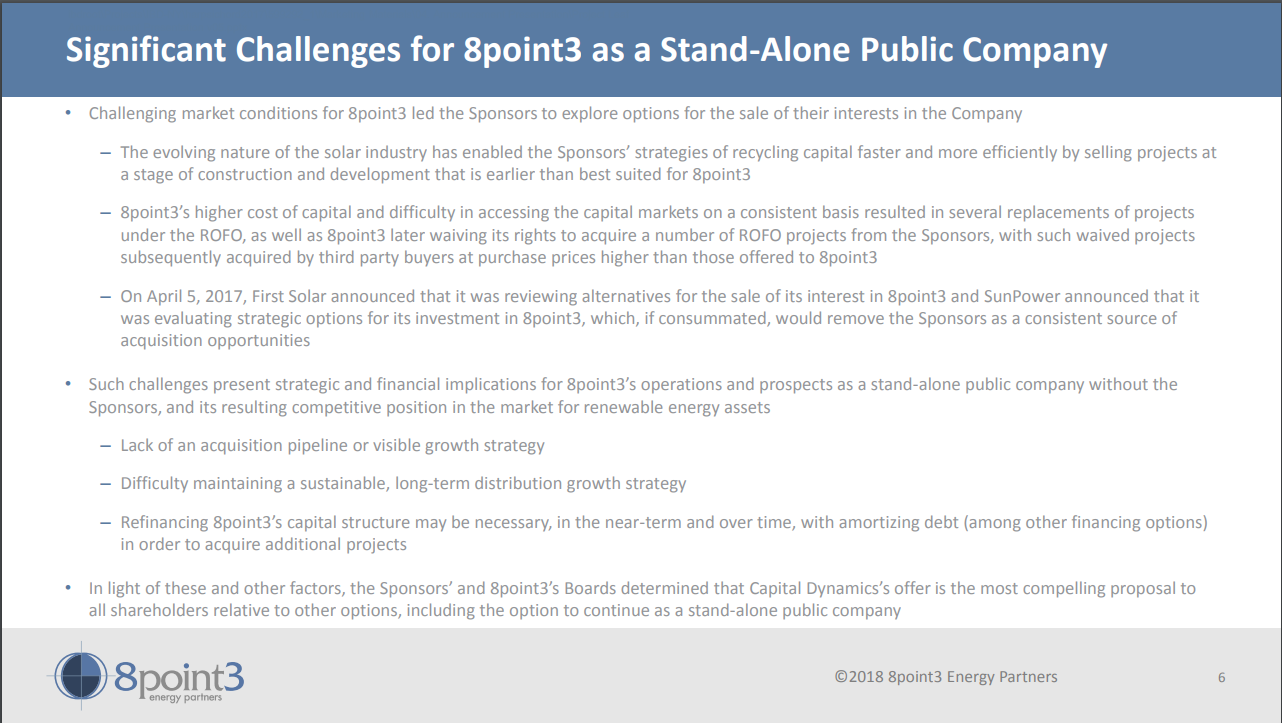

Slide 6 from 8point3 investor presentation.

What 8point3 wrote: “The evolving nature of the solar industry has enabled the Sponsors’ strategies of recycling capital faster and more efficiently by selling projects at a stage of construction and development that is earlier than best suited for 8point3.”

Translation: The 2017 downturn in solar installation meant that First Solar and SunPower need to sell solar farms quickly, often before they are completed. YieldCos like 8point3 typically buy solar farms after completion.

What 8point3 wrote: “8point3’s higher cost of capital and difficulty in accessing the capital markets on a consistent basis resulted in several replacements of projects under the [right of first offer], as well as 8point3 later waiving its rights to acquire a number of ROFO projects from the Sponsors, with such waived projects subsequently acquired by third-party buyers at purchase prices higher than those offered to 8point3.”

Translation: 8point3’s stock price is not trading at a large enough premium for it to sell shares to investors and invest in new solar farms while increasing the dividend. In short, investors are not willing to pay more for 8point3 shares than its current projects are worth. Unless First Solar and SunPower can sell projects to 8point3 at attractive prices, they have no reason to own it.

What 8point3 wrote: “Such challenges present strategic and financial implications for 8point3’s operations and prospects as a standalone public company without the Sponsors, and its resulting competitive position in the market for renewable energy assets:

Lack of an acquisition pipeline or visible growth strategy

Difficulty maintaining a sustainable, long-term distribution growth strategy

Refinancing 8point3’s capital structure may be necessary, in the near-term and over time, with amortizing debt (among other financing options) in order to acquire additional projects.”

Translation:

8point3 can’t grow in current market conditions

Our dividend growth is unsustainable

We have to refinance debt before 2020, and that would require a dividend cut

What 8point3 wrote: “In light of these and other factors, the Sponsors’ and 8point3’s Boards determined that Capital Dynamics’ offer is the most compelling proposal to all shareholders relative to other options, including the option to continue as a stand-alone public company.”

Translation: If shareholders reject this offer, they’ll regret it.

All of these risks have been clear to analysts (if not the investing public) since 8point3 started looking into refinancing its debt a year ago. What’s truly groundbreaking here is that these arguments are now being put forward by a YieldCo and its sponsors.

In 2017, 8point3 gave guidance for the year on the January 26, 2016 fourth-quarter conference call. It now looks like they delayed the 2017 fourth-quarter call in anticipation of this announcement. My 2017 analysis indicated that, without further acquisitions, 8point3 would likely see a slight decline in 2018 cash available for distribution.

Now that this deal has been announced, management has an incentive to release the bad news. I think we can expect plenty in the Q4 conference call, which, in turn, should get shareholders to vote for the deal.

The big picture

While many YieldCos have struggled since the popping of the 2015 YieldCo bubble, the discounted purchase price for 8point3 stock points more to specific problems at one company, rather than the YieldCo space in general.

On February 7, as this article was being written, NRG Energy (NYSE:NRG) announced the sale of its ownership stake in its YieldCo NRG Yield (NYSE:NYLD and NYLD/A) and its renewables development business and projects to global infrastructure investor Global Infrastructure Partners (GIP). On the same day, TerraForm Power (NASD:TERP) made an offer for Spanish YieldCo Saeta Yield (Madrid: SAY) at a 20 percent premium to the recent market price.

In contrast to the 8point3 sale, NRG Yield’s public shares are not being purchased. GIP will continue as a new sponsor of the public YieldCo, and is committed to NRG Yield’s future growth. In a press release, Adebayo Ogunlesi, chairman and managing partner of GIP, said, “We are…excited about the opportunity to grow the value of NYLD, which allows public market investors to access attractive investments in renewable energy.”

This echoes the sentiments of Brookfield Asset Management (NYSE:BAM) and Algonquin Power and Utilities (NYSE:AQN) in their recent purchase of sponsorship stakes in TerraForm Power and Atlantica Yield (NASD:AY) when those YieldCos’ respective sponsors filed for bankruptcy.

Most recent YieldCo sales have been a result of problems at the former sponsors, while 8point3’s sale is more a product of problems at the YieldCo itself. This is why 8point3’s shareholders are faced with selling at a discount, while shareholders of TerraForm Power and Saeta Yield received and/or are being offered a premium.

Stay tuned for a more in-depth analysis of the four recent YieldCo transactions and the state of the YieldCo space in general.

***

This article was first published on GreenTech Media.

Disclosure: Long TERP, AY, NYLD, NYLD/A, AQN. Short calls on CAFD. Short puts on FSLR (an effective long position). Tom Konrad and Jan Schalkwijk have an affiliation with the Green Income Folio, which is long TERP, AY, NYLD, NYLD/A and FSLR.

]]>https://www.altenergystocks.com/archives/2018/02/first-solar-sunpower-lobby-shareholders-sell-8point3-yieldco/feed/0Quick Take: Albemarle

https://www.altenergystocks.com/archives/2016/12/quick_take_albemarle/

https://www.altenergystocks.com/archives/2016/12/quick_take_albemarle/#respondSun, 11 Dec 2016 13:50:45 +0000http://3.211.150.150/archives/2016/12/quick_take_albemarle/Spread the love Tom Konrad, Ph.D., CFA Albemarle Corp. (NYSE:ALB) has come up twice in recent conversations with investment advisors in the last couple weeks. I’m not sure why the recent surge of interest, but I thought I’d share my email in response to the most recent query. An investment advisor friend: Any thoughts [on Albemarle]? […]

Albemarle Corp. (NYSE:ALB) has come up twice in recent conversations with investment advisors in the last couple weeks. I’m not sure why the recent surge of interest, but I thought I’d share my email in response to the most recent query.

An investment advisor friend:

Any thoughts [on Albemarle]? A mining company corners about 35% of the raw material for the manufacture of lithium batteries for electric cars.

My response:

I like it better than most Lithium plays, because they are vertically integrated. That said, I don’t like Lithium plays in general… seems similar to the whole rare earth thing. It’s likely to be a big boom and bust commodity cycle. Second, I just don’t like mining. On a valuation basis, ALB seems fairly valued, which means not nearly cheap enough for me. I also dislike the high beta. If you want to invest in cleaner transportation, my current top pick is MIXT.

Was that useful? Let us know in the comments, or if you have more in-depth thoughs on Albemarle.

]]>https://www.altenergystocks.com/archives/2016/12/quick_take_albemarle/feed/0The Week in Cleantech: Apr. 2 to Apr. 6

https://www.altenergystocks.com/archives/2007/04/the_week_in_cleantech_apr_2_to_apr_6/

https://www.altenergystocks.com/archives/2007/04/the_week_in_cleantech_apr_2_to_apr_6/#respondSun, 08 Apr 2007 12:51:47 +0000http://3.211.150.150/archives/2007/04/the_week_in_cleantech_apr_2_to_apr_6/Spread the love The Week in Cleantech is a weekly roundup of our favorite cleantech and alt energy blog posts and stories from across the web. If you know of a good piece that you think should be included here, don’t hesitate to let us know! This week, we particularly liked… On Monday, the Intergovernmental Panel […]

The Week in Cleantech is a weekly roundup of our favorite cleantech and alt energy blog posts and stories from across the web. If you know of a good piece that you think should be included here, don’t hesitate to let us know!This week, we particularly liked… On Monday, the Intergovernmental Panel On Climate Change issued its Fourth Assessment Report (AR4). Here’s an overview by the Green Car Congress. On Tuesday, Himanshu Pandya at Financial Nirvana informed us that certain Chinese solar companies believe that the silicon shortage is easing up. He shorted MEMC electronics [NYSE:WFR] because the shortage may be ending. On Tuesday, Emily Singer at Technology Review told us how a company was working to make biofuels better. Five years from now, the biofuels industry will be very different from today’s. On Tuesday, James Fraser at the Energy Blog reported on “the world’s first commercial solar tower power plant.” Pretty impressive! On Tuesday, Jack Brynaur at Quite Contrarian gave us a few options for profiting from blue gold. Water is a very interesting sector to watch and one which has largely fallen below the investor radar so far. Thanks to Seeking Alpha for this one. On Wednesday, James Fraser at the Energy Blog told us about Vinod Khosla’s venture investments. Always interesting to know what Khosla is up to. On Wednesday, Tom Whipple at The Energy Bulletin reported on the Government Accountability Office’s study on peak oil. In the article’s words: “[t]his report is clearly a milestone on our journey through the oil age for it is the first time the staff of a major government agency has looked at the issue and concluded that peak oil is real” On Wednesday, Mike Millikin at the Green Car Congress told us about a study on the outlook for biofuels in the Americas through 2020. Greater involvement in the biofuels business Latin American players is a near certainty, and essential if the US is to meet its aggressive targets. On Thursday, Worth Civils at WSJ’s Energy Roundup reported on a recent study on peak coal. That’s right, not peak oil – peak coal.

]]>https://www.altenergystocks.com/archives/2007/04/the_week_in_cleantech_apr_2_to_apr_6/feed/0Trade Stocks With Zero Commissions?

https://www.altenergystocks.com/archives/2006/09/trade_stocks_with_zero_commissions_1/

https://www.altenergystocks.com/archives/2006/09/trade_stocks_with_zero_commissions_1/#respondThu, 21 Sep 2006 12:42:24 +0000http://3.211.150.150/archives/2006/09/trade_stocks_with_zero_commissions_1/Spread the love Yes, the heading is right, zero commissions on trading stocks, not just low commissions. Zecco, a start-up allows consumers to trade stocks for zero commissions, versus $10 to $20 that many online brokers charge today. Morten Lund, on of the guys behind Skype, believes he can offer zero commission trading and recover costs […]

Yes, the heading is right, zero commissions on trading stocks, not just low commissions. Zecco, a start-up allows consumers to trade stocks for zero commissions, versus $10 to $20 that many online brokers charge today. Morten Lund, on of the guys behind Skype, believes he can offer zero commission trading and recover costs from advertising on the site. Let’s hope he is right. The launch of this appears to be in about 18 days. Full Story on Zero Commission Stock Trading at Zecco

]]>https://www.altenergystocks.com/archives/2006/09/trade_stocks_with_zero_commissions_1/feed/0Magnetek Announces Vanadium Redox Energy Storage System for Wireless Cell Sites

https://www.altenergystocks.com/archives/2006/04/magnetek_announces_vanadium_redox_energy_storage_system_for_wireless_cell_sites/

https://www.altenergystocks.com/archives/2006/04/magnetek_announces_vanadium_redox_energy_storage_system_for_wireless_cell_sites/#respondMon, 24 Apr 2006 18:50:56 +0000http://3.211.150.150/archives/2006/04/magnetek_announces_vanadium_redox_energy_storage_system_for_wireless_cell_sites/Spread the love Magnetek Inc. (MAG) and VRB Power Systems Inc. have announced the unveiling of a revolutionary 5kW Energy Storage System (ESS). Co-developed by Magnetek with VRB Power, the 5kW energy storage system is an alternative to traditional lead-acid battery backup systems. It provides cost effective, reliable, environmentally friendly, virtually maintenance-free backup power for wireless […]

Magnetek Inc. (MAG) and VRB Power Systems Inc. have announced the unveiling of a revolutionary 5kW Energy Storage System (ESS). Co-developed by Magnetek with VRB Power, the 5kW energy storage system is an alternative to traditional lead-acid battery backup systems. It provides cost effective, reliable, environmentally friendly, virtually maintenance-free backup power for wireless cell sites and other telecommunications facilities. Based on VRB Power’s patented Vanadium Redox Battery Energy Storage System (“VRB-ESS”), the 5kW system is comprised of an electrolyte storage tank containing a vanadium-based electrolyte supplied to a regenerative cell stack that converts chemical energy into electrical energy. A chemical reaction in the flow-cell stacks creates a current that is collected by electrodes and made available to an external circuit. This reaction is reversible, allowing recharging of the DC power modules. [ more ]

]]>https://www.altenergystocks.com/archives/2006/04/magnetek_announces_vanadium_redox_energy_storage_system_for_wireless_cell_sites/feed/0Ormat Technologies Signs Contract to Supply a Bottoming Cycle Power Unit to Geothermal Power Project in the Western Part of the United States

https://www.altenergystocks.com/archives/2006/04/ormat_technologies_signs_contract_to_supply_a_bottoming_cycle_power_unit_to_geothermal_power_project_in_the_western_part/

https://www.altenergystocks.com/archives/2006/04/ormat_technologies_signs_contract_to_supply_a_bottoming_cycle_power_unit_to_geothermal_power_project_in_the_western_part/#respondMon, 10 Apr 2006 08:38:04 +0000http://3.211.150.150/archives/2006/04/ormat_technologies_signs_contract_to_supply_a_bottoming_cycle_power_unit_to_geothermal_power_project_in_the_western_part/Spread the love Ormat Technologies (ORA) has signed a contract to supply a 10 MW Ormat Energy Converter (OEC) power unit. The contract is in the amount of $11,500,000. Since beginning operations in Nevada with the supply of a 760 kW geothermal plant in Lyon County, Ormat has supplied or installed approximately 800 MW of geothermal […]

Ormat Technologies (ORA) has signed a contract to supply a 10 MW Ormat Energy Converter (OEC) power unit. The contract is in the amount of $11,500,000. Since beginning operations in Nevada with the supply of a 760 kW geothermal plant in Lyon County, Ormat has supplied or installed approximately 800 MW of geothermal and recovered energy power plants in 23 countries, and has grown to own six U.S. geothermal facilities with a total of approximately 300 MW of generating capacity. The existing plant, to which an additional OEC will be added, uses single- flash technology to produce approximately 23 MW net of power to the grid. That plant utilizes only steam, which is separated from the brine and delivered to the plant, while the brine is reinjected into the ground. Ormat’s technology enables recovery of heat from the brine before reinjection and utilizes it to generate 10 MW of additional power in the Ormat Energy Converter (OEC) without additional resource or wells. The OEC power unit will be delivered in the second quarter of 2007 for installation adjacent to the existing plant. [ more ]

]]>https://www.altenergystocks.com/archives/2006/04/ormat_technologies_signs_contract_to_supply_a_bottoming_cycle_power_unit_to_geothermal_power_project_in_the_western_part/feed/0Are You an Alternative Energy Professional?

https://www.altenergystocks.com/archives/2006/03/are_you_an_alternative_energy_professional/

https://www.altenergystocks.com/archives/2006/03/are_you_an_alternative_energy_professional/#respondMon, 27 Mar 2006 14:42:12 +0000http://3.211.150.150/archives/2006/03/are_you_an_alternative_energy_professional/Spread the love As an AltEnergyStocks.com visitor, you’ve been invited to apply for a FREE one-year membership to the ChangeWave Alliance—the world’s most unique investment research network. If accepted for Alliance membership, you will get over $5,000 worth of investable research absolutely FREE! Members of the Alliance gain access to real-time, unbiased investment intelligence weeks ahead […]

As an AltEnergyStocks.com visitor, you’ve been invited to apply for a FREE one-year membership to the ChangeWave Alliance—the world’s most unique investment research network. If accepted for Alliance membership, you will get over $5,000 worth of investable research absolutely FREE! Members of the Alliance gain access to real-time, unbiased investment intelligence weeks ahead of the market. Accredited members also get a FREE one-year subscription to Tobin Smith’s ChangeWave Investing Advisory Service, plus exceptionally valuable research reports exclusively for Alliance members. In return, they participate a few minutes a month in surveys uncovering the latest technological and economic trends. You will find the interaction stimulating; the feedback useful; the benefits valuable; and the time commitment minimal. Plus it’s the most fun and rewarding membership of its kind. [ more ] The Alliance is looking to expand their coverage in the AltE space and are looking for people that work in the industry.